BloFin Research: Understanding the Priority of Bitcoin Sales During Market Risk Events

The post BloFin Research: Why BTC Gets Sold First During Risk Events appeared first on BeInCrypto.

During times of macroeconomic uncertainty, Bitcoin is often the first asset to be sold off. This trend can be attributed to its market structure, which is heavily influenced by perpetual futures that create a consistent long bias and positive funding rates. As a result, taking short positions becomes structurally easier and more cost-effective during periods of market stress.

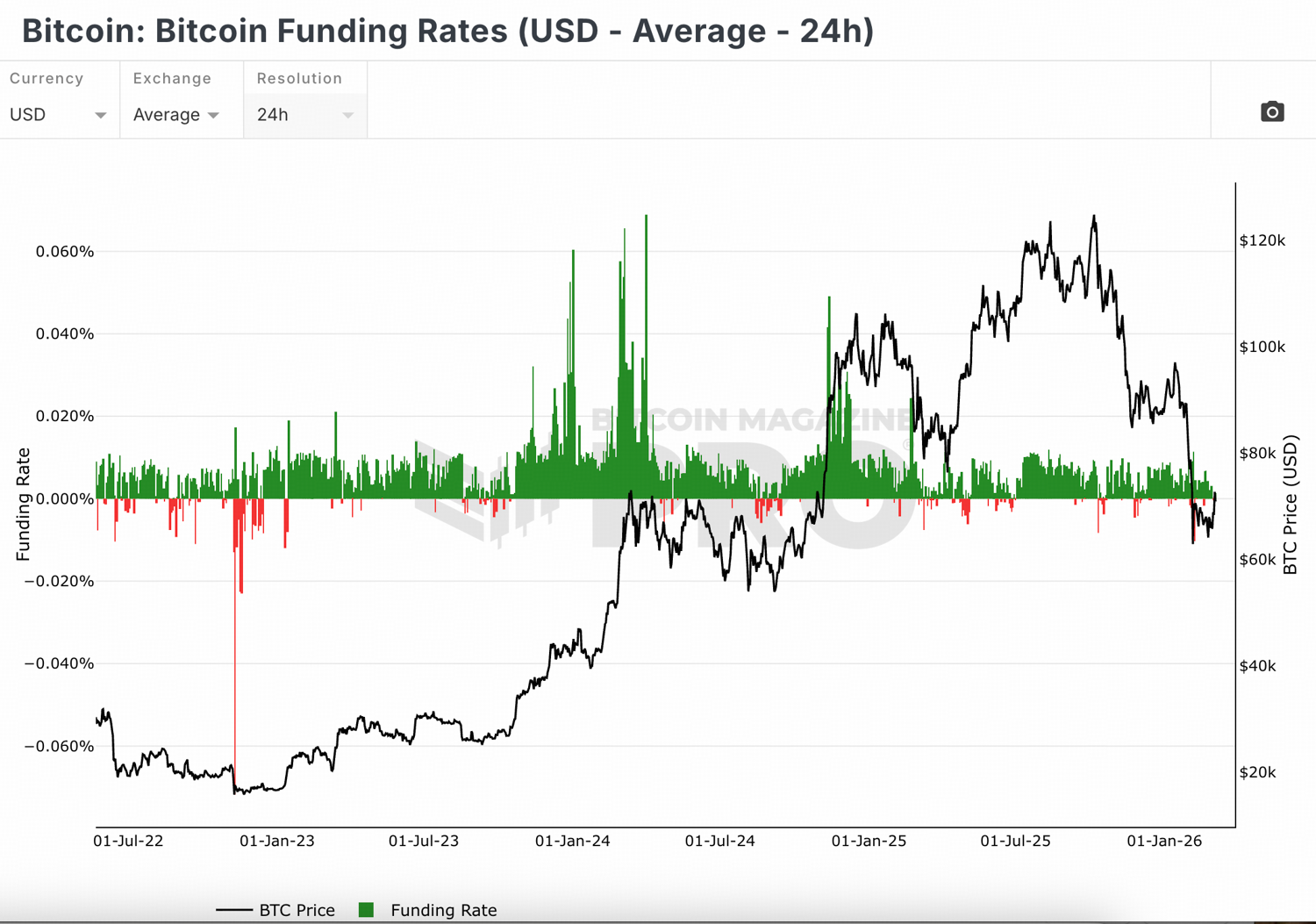

Since its launch, Bitcoin has maintained a bullish outlook in the Perpetual Futures market, with funding rates predominantly remaining positive (where longs compensate shorts). In contrast, gold typically sees an increase in value during such stressful economic events as investors flock to safe-haven assets. The selling of Bitcoin is less about its classification as a “risk-on” or “risk-off” asset and more about the underlying mechanics of perpetual funding.

The persistent positivity in Bitcoin’s funding means that any surge in long demand will further elevate these rates, thereby increasing the costs associated with maintaining long positions. Conversely, shorting becomes less expensive or even subsidized under these conditions. Thus, external pressures on the market tend to favor shorting rather than holding onto longs.

In our previous analysis regarding Bitcoin’s heightened volatility through the lens of market structure dynamics—characterized by speculative leverage and dominance from derivatives—we noted how this differs significantly from traditional commodities like Gold or Oil that operate within physically anchored frameworks with lower leverage ratios.

Article: Whale’s Digital Asset View: Why Bitcoin Sells Off While Gold Stabilizes

This piece delves into why Bitcoin consistently faces sell-offs ahead of other assets during widespread risk events—especially those occurring outside standard trading hours. As we previously mentioned, labeling Bitcoin merely as a “risk-on asset” provides little explanation for this behavior; instead we should ask:

Bitcoin meets all three criteria effectively.

The cryptocurrency derivatives landscape primarily operates through perpetual futures rather than fixed-term contracts. On major exchanges today, perpetual swaps dominate both volume and open interest due to their lack of expiration dates and continuous margin requirements; they serve as key instruments for quick positioning and price discovery within the crypto ecosystem. Typically speaking, movements in spot prices follow trends set by derivatives markets rather than leading them.

A defining feature distinguishing perpetual futures from traditional contracts lies within their unique funding rate mechanism: instead of converging towards spot prices upon expiry like conventional futures do; they remain tethered via periodic payments exchanged between longs and shorts based on current contract pricing relative to spot values. When trading above spot levels leads us into positive territory where longs pay shorts—and vice versa when below spot values create negative scenarios resulting in shorts compensating longs—this system perpetually aligns directional demands across traders’ interests.

Source: The Bitcoin Magazine

The chart illustrates how since inception until now there has been an overarching bullish sentiment toward bitcoin reflected through largely positive fundings (longs paying shorts) most days across prominent exchanges like Binance & Bybit indicating sustained willingness among participants opting for upside exposure despite potential volatility risks involved over shorter timeframes too!

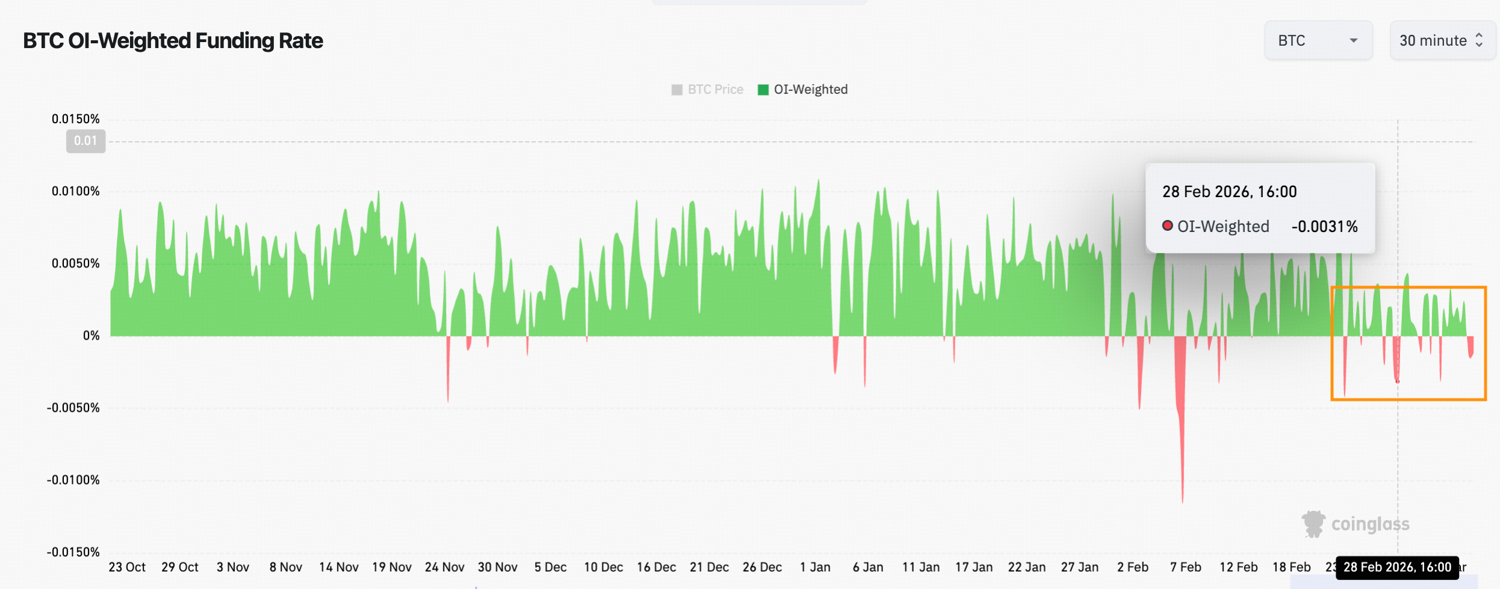

Source: Coinglass

Source: Coinglass