Bitcoin is entering a phase where macroeconomic sequencing takes precedence over storytelling.

Equity markets are trading at near-record valuations, real yields remain high, and credit markets are venturing into increasingly obscure areas of the financial landscape. While none of these factors guarantees an immediate downturn, they collectively set the stage for what could become a period of heightened volatility for risk assets.

The pivotal question for Bitcoin revolves around whether stress will arise in the financial infrastructure supporting inflated asset prices and how swiftly policymakers respond to mitigate it.

Macro strategist Michael Pento characterizes the current situation as a “triple bubble”: equities priced at historic highs, housing constrained by mortgage rates nearing 6%, and private credit approaching $2 trillion in assets under management. This label may be provocative, but it effectively highlights the importance of sequencing.

If credit begins to falter first, liquidity will dry up, leading Bitcoin to likely decline alongside other assets. Conversely, if policy support intervenes before any fractures occur, Bitcoin might act as a high-beta liquidity asset that rebounds more quickly than traditional risk investments.

The system rarely collapses solely due to stretched valuations; rather it breaks when issues within credit and bond markets force selling. Given Bitcoin’s continuous liquidity nature, it tends to react more intensely during both panic and recovery phases compared to almost any other asset class.

Recent data indicates that stress signals are accumulating without yet triggering significant disruptions.

The ICE BofA US High Yield option-adjusted spread was recorded at 2.95% on February 23—still tight compared to crisis levels.

The Federal Reserve’s balance sheet reached $6.613 trillion on February 18—a modest increase of approximately $28.8 billion over four weeks—indicating no emergency-level liquidity expansion is currently necessary.

Real yields measured by the 10-year TIPS yield hovered around 1.80% on February 20—high enough to exert pressure on non-yielding assets while stablecoin market capitalization stood at about $308.8 billion with only a slight decrease of -0.18% over thirty days—essentially flatlining overall performance.

Bitcoin reacts first; questions follow

A deflationary liquidation typically initiates within credit markets rather than equity indices themselves.

This results in widening high-yield spreads along with visible stress in funding markets; volatility surges while cash becomes the preferred position among investors seeking safety from risk exposure.

The behavior exhibited by Bitcoin during such periods tends toward predictability:

- Perpetual funding rates turn negative;

- Open interest declines sharply as leveraged positions unwind;

- Stablecoin supply contracts reflecting exiting liquidity;

- ETF outflows accelerate significantly during these times.

/

.. .. .. .

March 2020 serves as an illustrative historical reference point; during this time frame (specifically March 12), Bitcoin plummeted nearly 40%, mirroring declines across equities,credit,and commodities, driven largely by participants scrambling for dollar-denominated liquidities.

A liquidation stemming from credits can easily lead downwards movements ranging between -20% -40% (within just days).

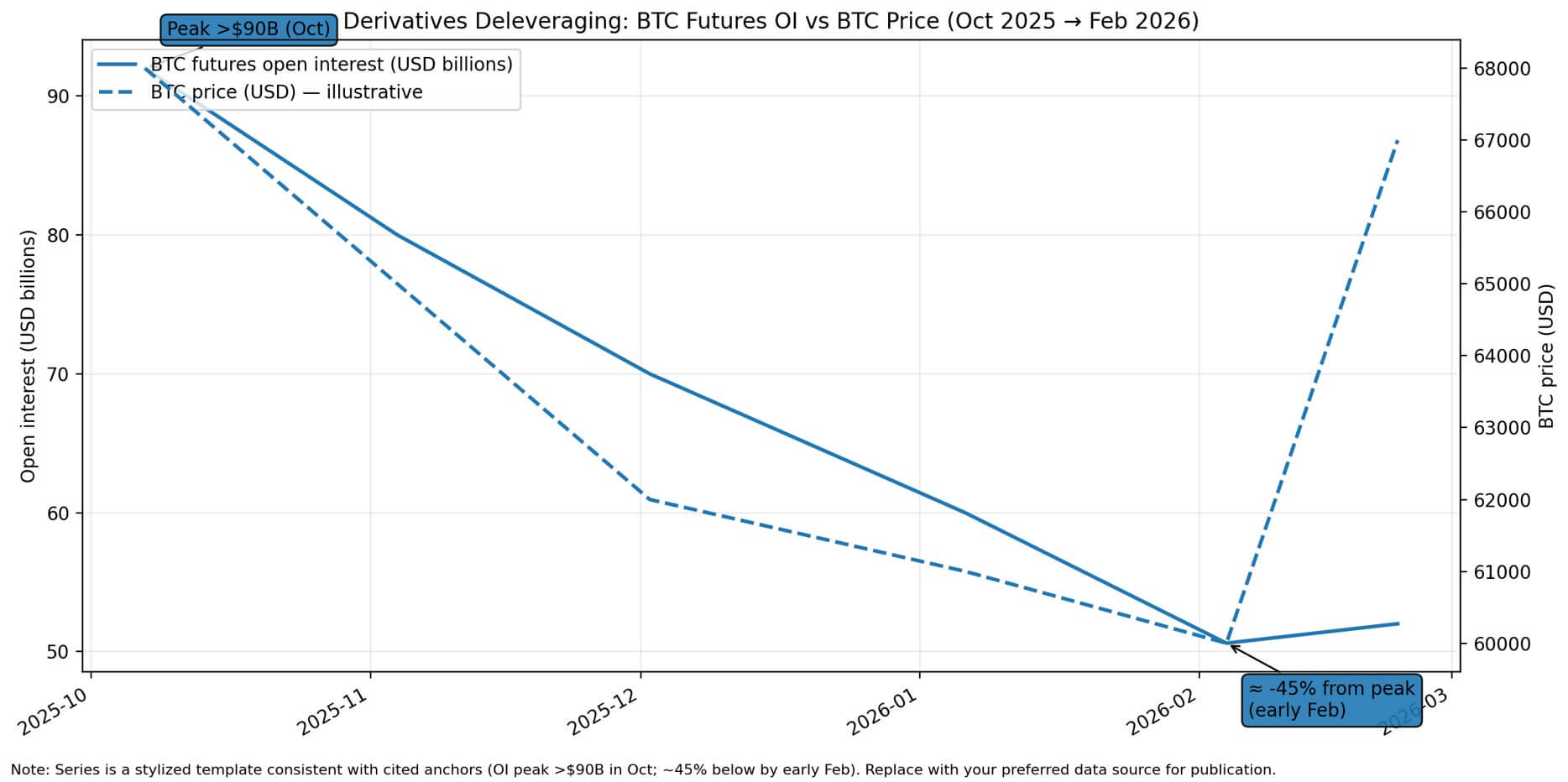

VanEck reported early February (2026): peak open interest regarding futures surpassed >$90 billion back in October; since then there has been an erosion exceeding -45% (from peak leverage levels), leaving room available should forced selling materialize amidst increasing pressures related specifically towards credits.

Moody’s anticipates private credit AUM surpassing >$2 trillion come and nearing >$4 trillion by year end (2030) – additionally highlighting Bank Of America’s commitment totaling $25 billion (in this sector).

This growth amplifies concentration risks associated with less transparent structures characterized through longer lockup periods coupled alongside weaker covenant protections.|

If any event occurs concerning credits which triggers forced sales across portfolios linked directly towards private sectors – repercussions would subsequently ripple throughout public marketplaces via collateral calls alongside margin pressures affecting them adversely.

Given its status being regarded as one among most liquid options available round-the-clock globally – hence absorbing disproportionate amounts resulting from selling activities occurring simultaneously!

“Bitcoin anticipates policy responses”

When visible supportive policies emerge—the opposite sequence unfolds entirely.

As Fed expands their balance sheets accordingly whilst establishing emergency facilities—we observe real yields decreasing consequently too! In such regimes where visibility exists regarding rescue efforts underway? Predictably enough…funding conditions normalize again while stablecoins’ supplies rise correspondingly indicating renewed influxes flowing back into crypto ecosystems! ETF flows stabilize or shift positively along with rebuilding open interests returning thereafter…

In environments characterized primarily through noticeable rescue actions taking place? Typically we see bitcoin behaving akin-to higher beta liquid trades recovering much faster relative-to conventional risky investments given absence surrounding inherent risks tied directly towards credits plus no earnings capable disappointing expectations either!

Referencing banking turmoil witnessed earlier (March ’23)—bitcoin surged upwards achieving +26% gains within just one week alone followed shortly thereafter (+40%) achieved altogether ten-day timeframe upon realizing shifting expectations pointing toward looser monetary policies ahead thus front-running eventual Fed interventions providing necessary support needed!

February ‘26 saw rapid fluctuations occurring whereby bitcoin oscillated dramatically rising beyond $70k all within single day showcasing largest uptick recorded since March ’23 emphasizing dominance still held firmly onto macro-risk sentiments prevailing amidst stressful windows observed previously mentioned earlier…

While events unfolding throughout March ‘20 depicted simultaneous collapses seen amongst various sectors—including however not limited exclusively towards banks—which eventually led Feds cutting rates down hitting rock bottom initiating unlimited quantitative easing measures enforced rapidly launching lending facilities aimed directly targeting emergencies encountered previously faced head-on!

Ultimately allowing BTC recover remarkably following lows established back then quintupled year after witnessing persistent fiscal spending surge onward amid continuing negative real yield environments sustained indefinitely long-term thereafter…

Overall takeaways suggest BTC operates highly responsive cycles surrounding respective liquefactions carrying notably higher betas compared against virtually every other existing asset presently traded globally thus timing proves critical surpassing mere narratives shared publicly amongst audiences alike here today…

“Navigating uncertainty when neither path prevails”

The most chaotic scenario arises wherein inflation remains stubbornly persistent whilst bond marketplace demands elevated term premiums leading ultimately restricting policymakers’ abilities delivering swift rescues without igniting fresh concerns relating specifically toward inflation itself further complicating matters substantially overall…

Under such circumstances? We witness fluctuating behaviors exhibited frequently throughout BTC trading patterns competing fiercely between both risk-off pressures clashing head-on against narratives advocating debasement hedging strategies simultaneously emerging concurrently challenging each other regularly…

Rallies tend fading fast once confronted consistently proving sticky realities concerning ongoing prevalent trends surrounding actual yields remaining firm despite potential supports failing deliver timely assistance promised beforehand originally planned instead ending disappointingly short ultimately falling flat…

Recent readings show current standings revealing neutral-negative atmospheres prevailing generally speaking now moving forward gradually evolving transitioning possibly soon into something else entirely different altogether depending greatly upon future developments transpiring next few months ahead potentially changing course taken here shortly afterward indeed!