Bitcoin’s downturn in the first quarter marked the end of an extraordinary period: nearly half a year of consistent underperformance compared to U.S. stocks, a phenomenon never seen before.

“This has never occurred previously,” explained Mark Connors, founder of Risk Dimensions, referencing data that highlights bitcoin’s persistent lag behind equities since early October. This ongoing trend has sparked renewed debate about whether bitcoin is acting more like a speculative risk asset rather than a protective hedge.

During Q1 2026, bitcoin dropped approximately 22%, following a 25% decrease in the last quarter of 2025. In contrast, the S&P 500 experienced significantly smaller losses over this timeframe, creating a notable performance disparity. Connors emphasized that it is not just the magnitude but also the duration of this gap that is remarkable; past declines were often steeper but lasted for shorter periods.

This weakness unfolded amid broader market challenges. U.S. stock markets endured their worst quarterly performance in four years, with the Nasdaq falling over 10% from its recent peaks. The combined downturn across both equities and cryptocurrencies wiped out much of the gains achieved after the 2024 election.

Progress on regulatory fronts has been mixed. The appointment of a new SEC chair facilitated smoother approval processes for crypto ETFs, while legislative efforts such as advancing the GENIUS Act have gained momentum. Additionally, former President Trump signed an executive order last August aimed at easing inclusion of alternative investments—including cryptocurrencies—in retirement plans like 401(k)s; subsequently, on Monday, the Labor Department proposed rules aligned with this directive.

Signs Of Resilience In March

Despite overall softness during Q1, bitcoin demonstrated greater resilience in March than many analysts anticipated.

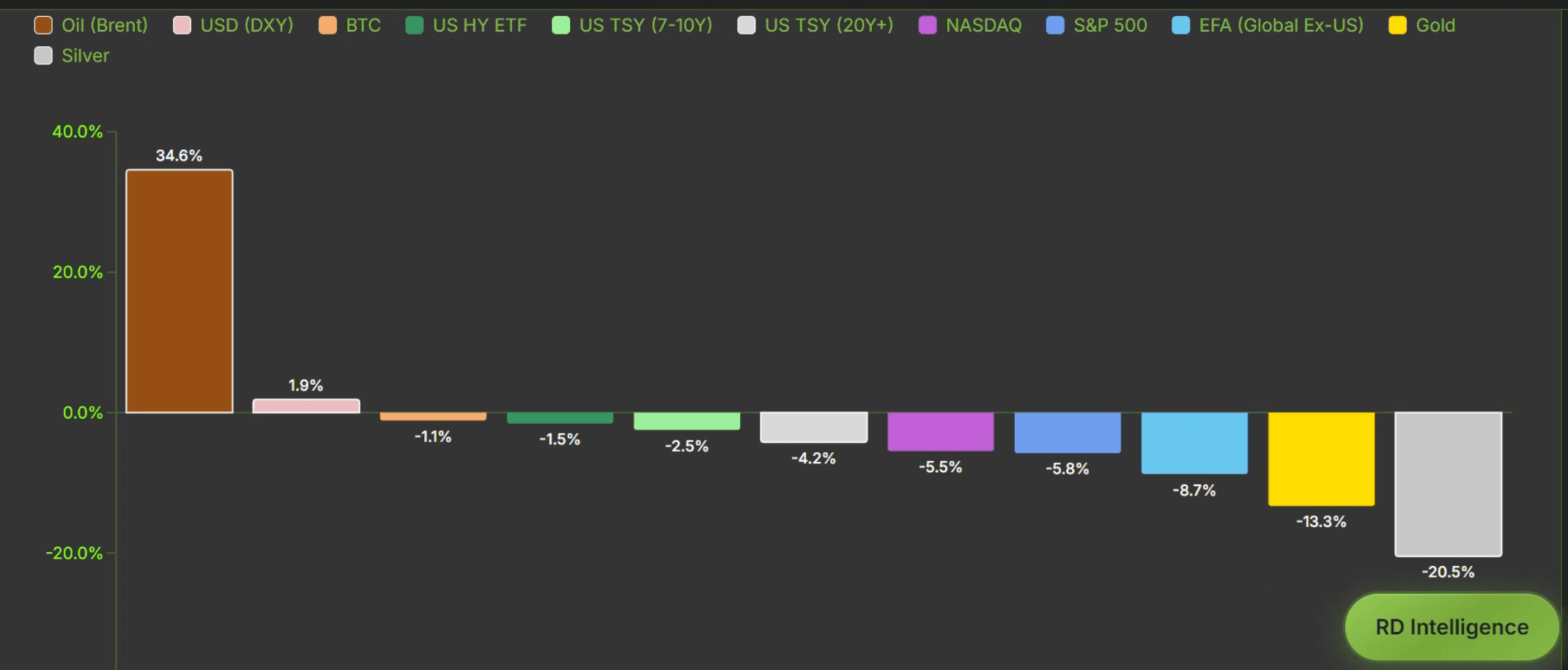

The escalation between U.S. and Iran early that month sent shockwaves through global financial markets—causing oil prices and dollar strength to surge as investors braced for supply disruptions and cost increases.

This volatility led to sharp fluctuations across various asset classes. Gold—traditionally viewed as a safe haven—experienced extreme price swings due to margin calls and urgent liquidity demands forcing sales by institutional players and sovereign funds alike; these moves ranked among some of the most severe short-term market dislocations seen in decades.

Conversely, bitcoin avoided similar forced liquidations: it gained roughly one percent throughout March while gold declined by eleven percent during that same period. “It really held steady,” noted Connors.

The relative stability can be partly attributed to prior liquidations which cleared leveraged positions earlier on Bitcoin’s network—and its inherent ability to transfer quickly across borders may reduce pressure-induced selling compared with tangible assets like gold or real estate.

A “Coiled Spring” Poised To Release?

Looking forward, Connors highlighted how Bitcoin’s prolonged underperformance against equities might influence future movements: rolling data over sixty-three days reveals it has trailed behind S&P500 returns since October—the longest recorded stretch—which historically signals potential upcoming reversals or rebounds.

If historical trends persist here too then Bitcoin could soon transition from relative weakness into renewed buying interest—especially given mounting macroeconomic pressures related to debt accumulation and currency expansion simmering beneath surface levels globally.

The exact timing though remains uncertain—it may hinge less upon structural market factors than geopolitical developments surrounding conflicts such as those involving Iran whose evolution will affect energy supplies liquidity conditions &; global risk sentiment profoundly .

&ldquo ; It could take either two months or two years , &rdquo ; concluded Connors .