On Friday, a significant event unfolded that underscores the rapid institutionalization of the bitcoin market, which has long been championed by individual investors.

This development is highlighted by the growth of options linked to BlackRock’s bitcoin exchange-traded fund (ETF), IBIT, which have recently surpassed total bitcoin options trading on Deribit in terms of size on Nasdaq. It’s noteworthy that within just two years, IBIT options have nearly matched Deribit’s bitcoin options market, which has been operational since 2016.

As reported by decentralized crypto volatility protocol Volmex, the dollar value of open or active IBIT options contracts on Nasdaq reached $27.61 billion on Friday—slightly exceeding Deribit’s $26.90 billion in bitcoin options.

This achievement signals that the U.S.’s regulated and institutional-grade infrastructure for investing in and trading derivatives related to bitcoin is now gaining prominence over offshore markets. Furthermore, a thriving regulated market in the U.S. could encourage more Wall Street institutions to delve into digital assets, potentially leading to enhanced price discovery mechanisms.

Sidrah Fariq, Global Head of Retail Sales and Business at Deribit, characterized IBIT’s ascent as beneficial for the entire crypto derivatives landscape.

“U.S. retail investors cannot access platforms like Deribit; therefore iShares Bitcoin Trust (IBIT) options provide them with direct access to regulated leverage and exposure through options,” Fariq explained to CoinDesk. “This trend is further bolstered by current macroeconomic conditions marked by supply chain uncertainties and geopolitical risks that naturally heighten demand for hedging strategies.”

Understanding Options

Options are derivative contracts granting buyers rights to purchase or sell an underlying asset at a predetermined price before a specified date arrives. Essentially it allows one party to reserve their right regarding future transactions at an agreed-upon price point—akin to paying a fee for this privilege now rather than later. A call option signifies buying rights while representing bullish sentiment; conversely, put options indicate selling rights.

The measure known as open interest reflects market size and participation levels—the greater this figure rises indicates deeper liquidity within markets.

Traders utilize these instruments not only as hedges against existing positions but also for speculation regarding price movements while generating additional income from their coin or ETF holdings.

A popular income-generating strategy involving both IBIT ETF and its associated call options is known as covered calls—allowing investors profit from $BTC‘s implied volatility while simultaneously holding ETFs alongside shorting calls well above current prices offered within those ETFs’ markets—a practice traders have employed via Deribit effectively over several years now!

A Comparison Between Markets

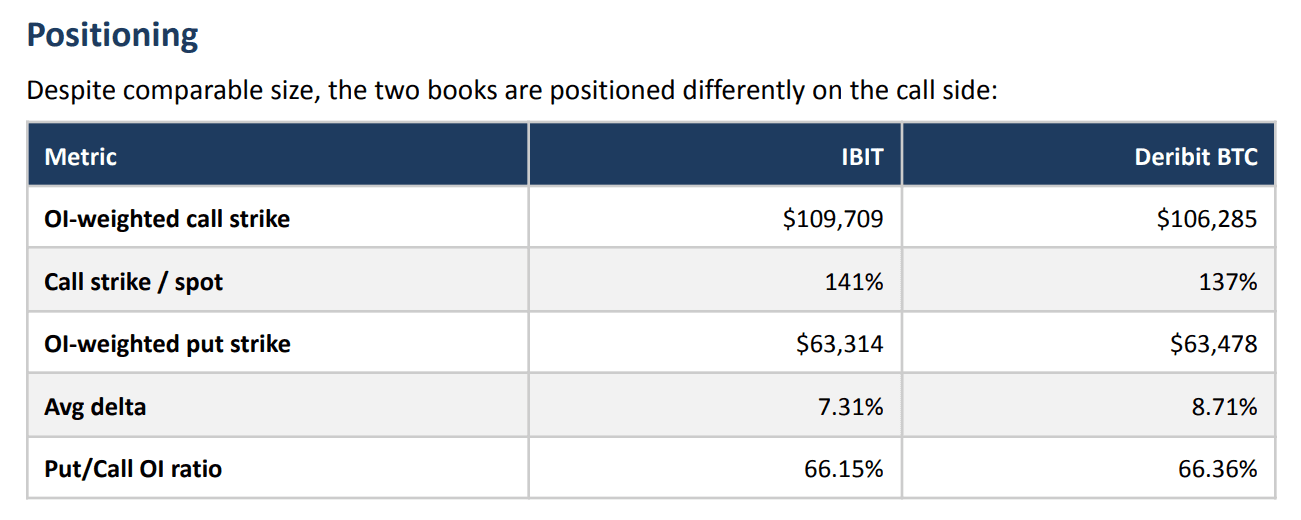

The two markets currently exhibit similar scales yet differ significantly in structure—a reflection revealing trader sentiments across each platform respectively!

The data provided by Volmex indicates that most open interest tied up with IBIT call-options suggests expectations around potential rallies pushing towards values equivalent near $BTC‘s trading levels reaching approximately $109709 shortly! This projection represents roughly forty-one percent above today’s prevailing rates ($77400).

Conversely positioning observed through derivative offerings seems optimistic albeit somewhat tempered indicating anticipations surrounding upward trends targeting closer towards $106000.

“Onshore call OI appears concentrated roughly four percentage points further out-of-the-money compared against offshore counterparts along with slightly lower average delta figures,” stated Volmex during its report shared earlier today via CoinDesk news outlet.

Pacing Among ETF Holders

Options possess expiration dates determining when contracts settle based upon prevailing rates associated either directly with spot $ BTC or respective funds themselves such as Ibit’s offerings.

Analysis comparing activity between both platforms reveals preferences leaning toward October 2026 expiries amongst participants engaging primarily through Ibit whereas August remains dominant among users opting into services provided via deribits network instead!

“IBit offers approximately two months longer-dated opportunities based upon OI-weighted assessments reflecting differing holder bases favoring longer-horizon investments versus tactical approaches taken offshore”, remarked volmex analysts noting key differences impacting overall strategies utilized throughout respective environments .

An additional observation found indicated higher implied volatility attached specifically relating back again towards ibits own metrics measuring expected fluctuations occurring over next four weeks compared against what was derived previously off deribits own offerings .

This premium arises due largely because holders lack ease when attempting short positions directly thereby relying heavily upon purchasing protective puts instead leading them ultimately keeping implied volatilities elevated consistently throughout ongoing developments seen thus far!

Taking everything discussed into account we see how rapidly ibit’s emergence has begun making waves across various sectors despite still being viewed differently altogether from traditional exchanges like deribits where global participants remain engaged fully outside regulatory confines typically imposed here domestically speaking however expanding opportunities available nonetheless will likely benefit all parties involved moving forward according Sidrah Fariq herself!”

FAQ:

- What are Bitcoin Options?

- If I buy an option contract do I need actual bitcoins?

- How does Open Interest affect my trades?

- You mentioned covered calls; can you explain how they work?

- Aren’t there risks involved when dealing with derivatives like these?